Bengaluru: Vedanta Limited today announced its Unaudited Consolidated Results for the Second Quarter and half year ended 30th September 2024.

2QFY25 Financial Highlights

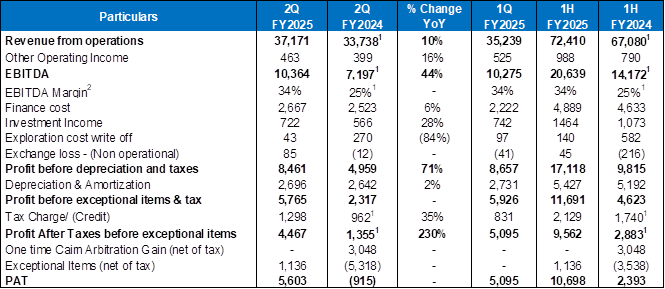

o Consolidated Revenue of ₹37,171 crore, up 5% QoQ and 10% YoY1.

o Consolidated EBITDA of ₹10,364 crore; 2nd Quarter in a row with 10k+ EBITDA, up 44% YoY1.

o Industry best EBITDA margin2 of 34%, up ~900 bps YoY1.

o Strong double-digit return on capital employed c.23%, improved ~152 bps YoY.

o Liquidity improved by 30% both QoQ & YoY with Strong Cash and Cash Equivalent of ₹21,727 crore.

o Generated Free Cash Flow (pre capex) of ₹8,525 crore up 50% YoY1.

o Net debt of ₹56,927 crore as on 30th September 2024, declined by ~₹4,400 crore vs June 2024.

o Net debt/ EBITDA at 1.49x in 2QFY25, marking the best position in last 6 quarters.

o Raised ₹8,500 crore through QIP and ₹3,133 crore through the Offer for Sale (OFS) of HZL.

o ICRA upgraded long term ratings from AA- to AA. Crisil Ratings revised outlook to ‘Watch with positive Implications’ from ‘Watch with Developing Implications’.

o Parent company, VRL, successfully raised $1.2 billion through a bond issue and reduced the interest costs on this debt by over 3%.

o Net Debt at parent entity reduced by $1bn in first half to reach to its lowest level in a decade.

o Demerger on track and in its final stages, with shareholder and creditor meetings scheduled in the coming months.

2QFY25 & 1HFY25 Operational Highlights

Below are the key operational highlights across the Group during the Quarter & Half Year:

All-time high first-half outputs across key businesses; new production benchmark while continuing to spearhead India’s industrial progress and energy shift.

§ Aluminium

o All time high first half Cast Metal production at 1205 kt, up 3% YoY.

o Highest ever Cast Metal production of Aluminium at 609 kt up 2% QoQ & 3% YoY.

o Aluminium cost of production at 1734$/t down 4% YoY.

o Alumina production at 499 kt up 8% YoY.

§ Zinc India

o All time high first half Metal production at 524 kt, up 5% YoY.

o Highest-ever mined metal & refined metal production in second quarter at 256 kt, up 2% YoY and 262 kt, up 8% YoY.

o Zinc COP at 1071$/t down 6% YoY and 3% QoQ, marking the lowest 1H cost in last 4 years.

§ Zinc International

o Lowest ever Quarterly COP for Gamsberg at $1125/t.

o ZI cost at 1195$/t down 13% YoY and 26% QoQ, Lowest since Q1 FY17.

§ Oil and Gas

o Average daily gross operated production of 104.9 kboepd, natural decline was partially offset by the infill wells brought online in Mangala and RDG fields.

o Volumes at OALP arrangement rise to 4.0 kboepd vs 1.0 kboepd YoY, supported by ramp-up of Jaya Oilfield.

§ Iron ore

o Saleable ore production at 1.3 million tonnes, up 7% YoY and 3% QoQ .

§ Steel

o Production adversely impacted due to the planned shutdown on account of the debottlenecking of Steel Melting Shop and maintenance of Oxygen Plant in 2Q.

§ Facor

o Ferro Chrome Ore production at 38 kt ~2x YoY, Ferro Chrome production at 26 kt up 18% YoY.

§ Copper India:

o Copper Cathodes production at 41 kt doubled in QoQ & up16% YoY.

o Tuticorin Smelting operations have remained halted since April 2018. The company is evaluating the legal remedies for sustainable restart of Tuticorin plant.

Executive comments:

Commenting on 2QFY25 results, Arun Misra, Executive Director Vedanta Limited said, “Vedanta is proud to report our highest-ever first-half EBITDA of ₹20,639 crore with 46% growth YoY1. The second half of this year will be a transformative period with our major growth and integration projects coming online and ramping up. Through our structural interventions and initiatives, we have significantly reduced our cost of production over the past 12-15 months, and we will continue this trend in the coming quarters. As we move forward, operational excellence, sustained growth, and ESG leadership remain our strategic priorities. With a rich, diversified asset portfolio, a stronger balance sheet, and ongoing growth projects, we are well-positioned to deliver exceptional overall performance.”

Ajay Goel, CFO, Vedanta Limited, said “This has been an outstanding quarter, highlighted by significant progress in our corporate and strategic initiatives, strong financial results, and excellent operational performance. We delivered our highest-ever 1H EBITDA of ₹20,639 crore, up 46% YoY1, with a robust 34% EBITDA margin and PAT before exceptional items of ₹4,467 crore, a 230% YoY1 increase. This strong performance is driven by cost efficiency, volume growth, and favourable commodity prices. Additionally, we raised $1.4 billion at Vedanta through a $1 billion QIP and a $400 million HZL OFS. At the same time, with the $1.2 billion VRL bond issuance and ongoing deleveraging, we have reduced Holdco. debt to $4.8 billion, the lowest level in a decade. This positions us well to generate lasting value for our stakeholders, both now and in the years to come.”

2QFY25 ESG Highlights

§ Renewable Energy (RE): Secured RE Power Delivery agreements (PDAs) of 1906 MW (+80MW QoQ). Initiated utilization of renewable energy in line with RE PDAs at Zinc India and Aluminium Business.

§ Gender Diversity: Achieved our workplace gender diversity target for full-time employees 7 years in advance vs FY30 target of 20%. Gender diversity for full-time employees stands at 22% (FY24: 20%)

§ ESG Rating: Secured top three ranking in the S&P Global CSA assessment in 2024, for second consecutive year.

§ CSR: Spent INR 141+ crore in 1HFY25 on CSR initiatives for communities, positively touching over 3.5 million lives

§ Women & Child Welfare: 6,363 Nand Ghars created for women and child welfare

Consolidated Financial Performance –

1. Comparatives exclude impact of one-time cairn arbitration gain in 2Q FY24.

2. Excludes custom smelting at copper business.

§ Revenue:

o 2QFY25 consolidated revenue up 10% YoY1 majorly due to favourable output commodity prices, increased volume and premia.

o 2QFY25 consolidated revenue at ₹37,171 crore, up 5% QoQ majorly due to increased volume & premia, partly offset by lower output commodity prices.

§ EBITDA and EBITDA Margin:

o 2QFY25 EBITDA increased by 44%1 YoY to ₹10,364 crore majorly due to favourable output commodity prices, structural cost saving initiatives and increased premia across businesses.

o 2QFY25 EBITDA increased by 1% QoQ majorly due to increased volume, structural cost saving initiatives & increased premia, despite lower output commodity prices.

o EBITDA margin1 at 34% in 2QFY25, improved ~900bps YoY1.

§ Depreciation & Amortization:

2QFY25 Depreciation & Amortization ₹2,696 crore increased 2% YoY mainly in Oil & Gas and increased capitalization at Aluminium.

§ Finance Cost:

o 2QFY25 in line with average borrowings; 1QFY25 lower due to one-time item.

o 2QFY25 higher by 6% YoY in line with increase in average borrowings

§ Investment Income:

o 2QFY25 higher by 28% YoY due to increase in average investments.

o 2QFY25 lower by 3% QoQ due to one-time gain in 1QFY25.

§ Taxes:

Normalized ETR (excluding exceptional items) for 2QFY25 is 27% as compared to 26% in 1QFY25. Increase is mainly due to change in profit mix.

§ PAT before Exceptional Items:

2QFY25 PAT before Exceptional Items at ₹4,467 crore, higher 230% YoY1.

§ Exceptional Items:

2QFY25 Exceptional Gain of ₹1,136 crore majorly due to impairment reversal in Oil & Gas business partly offset by impairment charge in ASI, and Cess in zinc & iron ore vide Supreme Court judgement to levy additional Cess on mineral-bearing land & mining rights.

§ PAT:

2QFY25 PAT of ₹5,603 crore, higher 10% QoQ.

§ Leverage, liquidity, and credit rating:

o Gross debt at ₹78,654 crore as on 30th September 2024.

o Net debt at ₹56,927 crore as on 30th September 2024. Net debt to EBITDA ratio improved to 1.49x marking the best position in last 6 quarters.

o Cash and cash equivalents position remain healthy at ₹21,727 crore, increased by 30% both QoQ and YoY. The Company follows a Board-approved investment policy and invests in high quality debt instruments with mutual funds, bonds, and fixed deposits with banks.

o Additionally, ICRA has upgraded our long-term ratings from AA- to AA. Also, Crisil Ratings had revised outlook on the long-term ratings to ‘Watch with positive Implications’ from ‘Watch with Developing Implications’ while reaffirming the ratings at ‘CRISIL AA-‘.

2QFY25 Awards and Recognitions –

§ Taxation:

o HZL honoured by the Rajasthan GST Department for being Rajasthan’s 2nd Highest Taxpayer

o HZL won GST Compliance Excellence Award at the 8th Tax Strategy & Planning Summit & Awards 2024.

§ Safety:

o Cairn India- Ravva won Second Prize in the DGMS Mines Safety Week 2004

o BALCO achieved Four Stars in British Safety Council Five Star Audit 2024

§ Business Excellence:

o BALCO won National Award for Digitalization by CII.

o Triple Recognition for Vedanta Lanjigarh at CII National Energy Efficiency Circle Competition 2024.

§ Sustainability:

o Rampura Agucha and Sindesar Khurd mines were awarded the prestigious 5-Star Rating from the Indian Bureau of Mines for outstanding implementation of Sustainability Development Framework.

o Vedanta Jharsuguda bags National Award for Energy Excellence 2024.